What Should I Do With My TSP After I Retire?

If you have a TSP and are a Federal employee nearing retirement, you are probably wondering exactly this question. Before you retire, it is wise to be proactive and plan for retirement. How are you going to make up for lost income? How can you pay the least possible in taxes every year? Do you have enough saved for retirement, or do you need to work longer, even if it is part-time?

Whatever you decide to do with your TSP depends specifically on your personal needs and situation. There is no cookie cutter answer on the best option for someone, but you want to make sure you take full advantage of all the benefits a Thrift Savings Plan has to offer. We suggest thinking through your options and seeking professional guidance before making a final decision.

Now, we will address 4 options to your question, “What should you do with your TSP after you retire?”

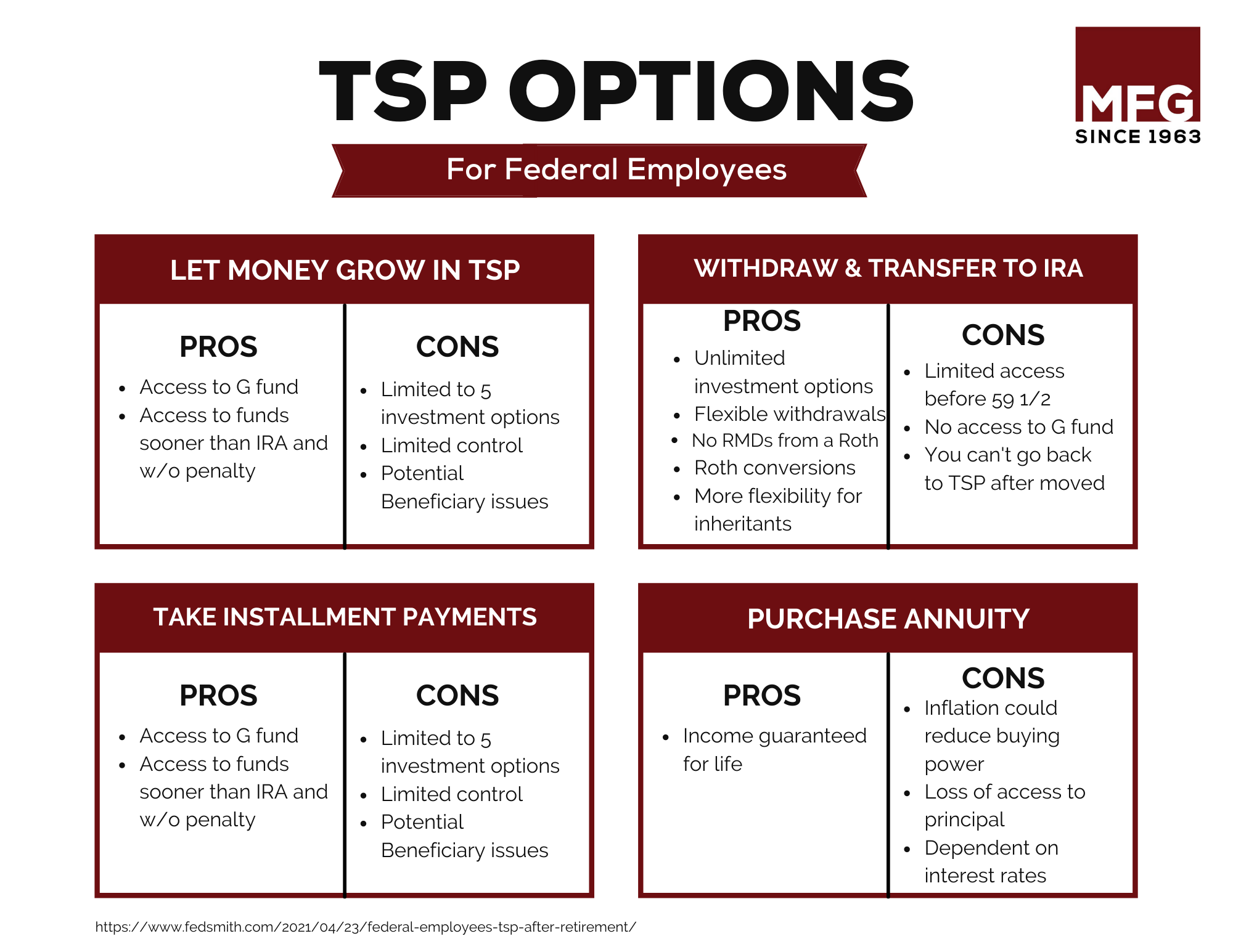

1. Let money grow in the TSP

You have the option to leave your account balance in your TSP if you aren’t required to take minimum distributions (age 70 ½ +) or your balance is more than $200 when you leave federal service. By leaving the money in the TSP, you can enjoy tax-deferred earnings and low expenses. However, you will not be able to make employee contributions anymore.1 You also have the chance to change your investment mix and transfer money into one of your accounts, if eligible.

2. Withdraw & Transfer TSP to an IRA

A lot of the time, this is the option we recommend most to clients. By transferring the account over to an IRA, you have greater control and freedom.2 With this control, you have the option to shop around and purchase an annuity if you want or let the funds sit and grow if the money isn’t needed immediately, without the limitations of a TSP. You are able to research and choose investment options that coincide with your goals and risk tolerance.

However, it’s critical that you speak with a professional before transferring your TSP because you want to make sure you do it correctly to avoid any tax consequences.

3. Take Installment Payments

Another option you have with your TSP is to receive regular payments monthly, quarterly, or annually.1 The withdrawals will continue to come from your TSP until the money runs out.5

Normally, Federal employees need to wait until age 59 ½ to begin withdrawals without incurring a penalty. 2 However, there are exceptions for Special Category Employees such as law enforcement and others. When you take these installment payments, you may have tax implications depending on the type of contributions you made. If your TSP was Traditional, you made contributions with pre-tax dollars, meaning you will need to pay income taxes on the distributions. If you contributed to a Roth TSP, the distributions will be tax free.

If you would like help understanding the tax implications of your TSP in retirement, speak with a tax or financial professional.

4. Purchase an Annuity

If you’re wanting guaranteed income in retirement for the rest of your life, you have the option to use your TSP balance to purchase an annuity that can do just that. It can be a way to give you comfort and security in retirement, where all you have to do is wake up and that money will be there. Payments with annuities are usually monthly, and the value of the amount you receive will depend on your total TSP balance.

However, these often have a cost to them. Be sure to speak with a professional to fully understand what you’re getting into before you decide on this option.

Here is a summary of the pros and cons of each option.

Before it is time for you to retire, we suggest going over what you can do with your TSP with a financial professional. Looking at your whole financial picture, they will be able to guide you down the path that is best for you and achieving your goals. It is critical to get guidance, though, as a mistake can cost you thousands on penalties or taxes that could otherwise be avoided.

Reach out to us if you have questions about your TSP.

SOURCES: