How to Fund an Unexpected Expense

After the craziness of the last few years. I think we all know life throws curveballs you never expect, and you can never plan perfectly for. Even if you have done comprehensive financial planning, there is no way to avoid unforeseen circumstances. Life happens and all the sudden you might be faced with an unexpected expense that you weren’t prepared for, and you’re stuck scrambling to try to find a way to pay for it.

We want you to know you’re not alone. There are ways to address the unexpected expense, whatever it’s from, to minimize the impact it has on you, your family, and your financial goals. There are a few key issues to consider when you must fund an unexpected expense: payment strategies, funding sources, tax consequences, and the overall impact on your financial plan.

Payment Strategies

First, you need to understand the terms of the expense. Ask yourself these questions:

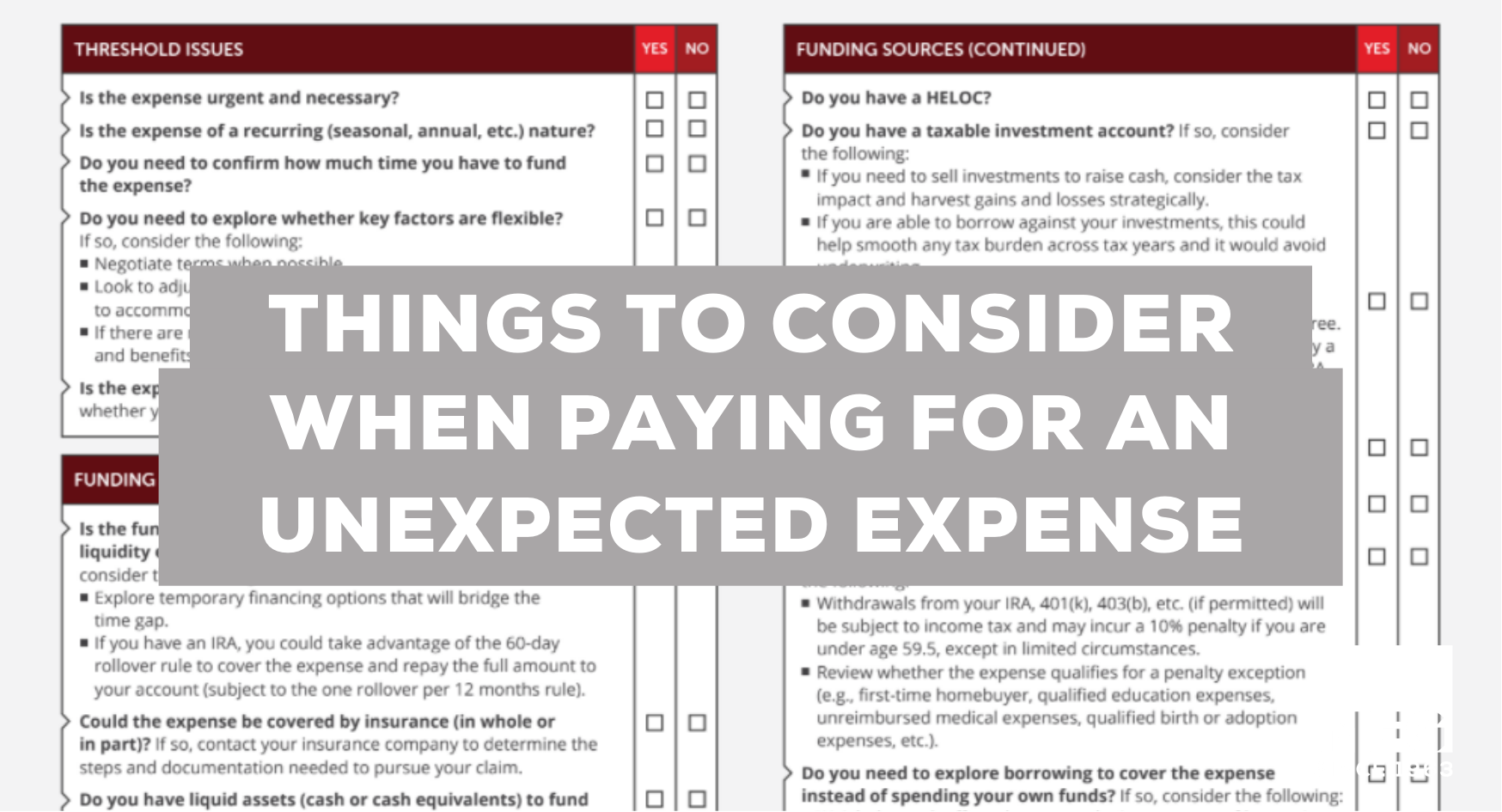

- Is the expense urgent and necessary?

- Is the expense of a recurring nature (seasonal, annual, etc.)?

- How much time do you have to fund the expense?

- Are key factors flexible?

- If so, try and negotiate the terms

- Depending on your circumstance, look to adjust your timeline for making payments

- If there are more affordable options, weigh the pros and cons to make an informed decision.

Funding Sources

The next step is figuring out where to get funding.

Do you need funding only for a short time? For example, you expect a future liquidity event will eventually cover the expense. If so, consider these options:

- Research temporary financing options that will bridge the time gap.

- If you have an IRA, you can use the 60-day rollover rule to cover the expense and repay the full amount to your account. *

Here are more funding sources to consider:

- See if the expense can be partially or fully covered by insurance.

- If you have liquid assets, consider using those and then come up with a savings strategy to replace the lost liquidity.

- Do you have a taxable investment account?

- If you need to sell investments to raise cash, consider the tax impact and harvest gains and losses strategically.

- Do you have a Roth IRA?

- Contributions can be withdrawn at any time, tax, and penalty free. However, withdrawn earnings may be subject to income tax and possibly a penalty. Make sure you’re considering the impact on your long-term financial plan and consult with your tax professional.

- Explore borrowing to cover the expense instead of spending your own funds.

- Weigh the pros and cons and compare interest cost of borrowing: compared to the opportunity cost of spending rather than investing your own assets

- Research any financing options through the vendor/service provider.

- If the need is short term, consider using a credit card with a 0% intro APR to pay for the full expense. This way, you can have time to pay off the balance over the favorable interest rate period.

See this checklist for more funding options.

Tax Consequences

Depending on what the unexpected bill is, there could be potential tax issues that you also need to consider. However, if the unexpected expense is a tax bill, you can adjust withholdings or estimated payments throughout the year.

Here are some other tax issues to consider:

- Are you withdrawing funds from a tax-preferred account (529 plan, HSA, etc.)?

- Consider the tax impact and any potential penalties. Make sure to keep accurate records.

- Will you borrow to fund the expense?

- Research whether any interest payments will be tax-deductible.

- Is it a home improvement expense?

- Make sure to keep proper records to document any increase in your cost basis.

- If you have the option to control the timing of the expense, does it make sense to delay into the next tax year or to spread across multiple years?

See other potential tax issues on this checklist.

Impact on Financial Plan

An unexpected expense can potentially have repercussions on your financial plan. Whether you had to dig into your emergency fund or take a loan out, you might need to readjust your budget in order to replenish your savings or cut out unnecessary expenses so you can make loan payments.

Reassess your discretionary spending and eliminate unnecessary costs to free up funds and redirect savings. Instead of taking a vacation next month, maybe wait a while until you have a better handle on your financial situation.

If you did incur debt to cover the expense upfront, do you need a debt reduction or consolidation plan? If you do, treat repayments as a fixed expense in your budget moving forward. After you have the expense taken care of, it is smart to consider how you can replenish your emergency savings.

Unexpected expenses can be extremely stressful but also can’t be avoided. It’s important to research all your options, weigh the pros and cons, and choose the best option for you and your family that will have the least impact on your long-term goals.

If you’re looking for more information on this topic, download this checklist: What Issues Should I Consider when Funding an Unexpected Expense? Also, it’s always a good idea to seek out professional guidance. If you have questions or would like to talk more, please contact us at 712-623-5726 or book an appointment on our calendar.

*While this is an available option for funding a very short-term expense, please be aware that should the full amount not be repaid within 60 days taxes and early withdrawal penalties may apply. Additionally, individuals are allowed 1 rollover per calendar year.